What’s the Difference and Which is Best?

When you are facing an urgent financial shortage, navigating the world of online lending can feel overwhelming. You will repeatedly run into two primary options for fast funding: payday loans and installment loans.

While both options provide quick cash to cover unexpected gaps, they operate on completely different frameworks. Choosing the wrong one can lead to a compounding cycle of high-interest debt. This comprehensive guide breaks down the technical details, costs, and structural differences to help you make an informed financial decision.

What is a Payday Loan?

A payday loan is a short-term, high-cost financial instrument designed to act as a bridge until your next paycheck arrives. These are typically small-dollar loans ranging from $100 to $1,000.

How Payday Loans Work:

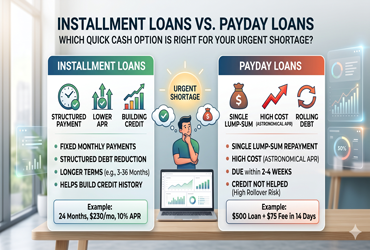

Repayment Structure: Unlike traditional loans, a payday loan does not have monthly installments. The entire principal balance, plus interest and fees, must be repaid in a single lump sum, typically within 2 to 4 weeks (on your next payday).

The Payment Mechanism: Borrowers usually write a post-dated check for the full amount owed or authorize the lender to electronically withdraw the funds directly from their checking account on the due date.

Credit Requirements: Payday lenders rarely perform a traditional hard credit check. Approval is primarily based on proving you have an active checking account and a steady source of income.

⚠️ The True Cost of Payday Loans:

Because these loans are meant to be paid back quickly, lenders charge flat fees instead of traditional interest rates (e.g., $15 for every $100 borrowed).

When calculated as an Annual Percentage Rate (APR) to show the true yearly cost, a typical payday loan carries an astronomical APR of 300% to 500%.

What is an Installment Loan?

An installment loan is a much more structured form of borrowing. It allows you to obtain a lump sum of cash up front and pay it back over a fixed timeline through a series of scheduled, equal payments (installments). This category includes personal loans, auto loans, and specialized bad credit installment loans.

How Installment Loans Work:

Repayment Structure: Instead of demanding the full amount back at once, installment loans split your balance into predictable monthly or bi-weekly payments spread over several months or years (typically 3 to 36 months for online consumer loans).

Amortization: Each payment you make is split into two parts: one portion goes toward paying off the interest, and the remaining portion goes toward reducing the principal balance.

Credit Requirements: Lenders vary significantly here. Mainstream banks look for good credit, while online subprime installment lenders look closely at alternative data like employment history, residual income, and banking stability.

The True Cost of Installment Loans:

The APR on an installment loan is heavily dependent on your credit score and state regulations.

Prime Borrowers: Can see APRs between 6% and 15%.

Subprime/Bad Credit Borrowers: May face APRs ranging from 25% to 99%, depending on the lender type and local state interest rate caps.

Key Differences: Head-to-Head Comparison

To understand exactly how these options contrast, look at this breakdown of their core mechanics:

| Features & Mechanics | Payday Loans | Installment Loans |

|---|---|---|

| Typical Loan Amounts | $100 to $1,000 | $1,000 to $5,000+ |

| Repayment Period | 14 to 30 days (Lump sum) | 3 to 36+ months (Equal payments) |

| Average APR Range | 300% – 500% | 6% – 36% (Up to 99% for subprime) |

| Credit Bureau Reporting | Rarely reports positive payments | Frequently reports to Equifax/Experian |

| The Debt Trap Risk | High (Due to rollover/refinancing) | Moderate (Easier to budget fixed amounts) |

The Danger Zone: Rollovers vs. Amortization

The biggest fundamental difference between these two options is what happens if you cannot pay the money back on time.

The Payday Loan Rollover Trap

If you cannot afford to pay back a $500 payday loan plus fees on your next payday, many lenders allow you to "roll over" or renew the loan.

Example: You pay only the fee to extend the loan for another two weeks. Now, you still owe the original $500, but a second round of high fees is tacked on. This structure makes it incredibly easy to pay hundreds of dollars in fees without ever lowering the actual amount you borrowed.

🚀 The Installment Loan Safety Buffer

- Because an installment loan builds principal reduction into every single scheduled payment, you are guaranteed to be completely debt-free by the end of the loan term, provided you make your payments on time. There is no need to constantly renew or roll over the balance.

Which Option Suits Your Situation Best?

While saving an emergency fund is always the ideal path, if you must choose an online financing option immediately, use these guidelines:

Consider a Structured Installment Loan if:

You need more than $1,000: Splitting a larger amount into monthly pieces makes it affordable.

You need room in your budget: Predictable, fixed monthly installments prevent your entire upcoming paycheck from being wiped out.

You want to build credit: On-time payments reported to the major credit bureaus will help improve your credit profile over time.

Consider a Short-Term Payday Loan Only if:

You have absolutely no other choice: Every other line of credit or alternative has failed.

The amount is very small: You only need $200 or $300 to buy groceries or gas before Friday.

You are 100% certain you can pay it off: You have guaranteed funds hitting your account on payday to wipe out the debt completely in one shot, avoiding the rollover trap.

FAQs

Q: Does an installment loan hurt your credit score more than a payday loan?

A: No. Applying for an installment loan may trigger a temporary, minor drop due to a hard credit inquiry. However, making your monthly installment payments on time is an excellent way to boost your credit score over the long term. Payday loans generally do not report to credit bureaus at all, meaning they cannot help build your credit.

Q: Can I pay off an installment loan early?

A: Most reputable online lenders allow you to pay off your balance early without any prepayment penalties. Doing this saves you a massive amount of money on interest because it cuts the amortization cycle short.

Q: Why are payday loan APRs so high compared to installment loans?

A: Payday loans compress their fees into a very short timeline (2 weeks). When you mathematically calculate a 15% flat fee over just 14 days and compound it across an entire 365-day year, the structural math forces the APR into triple digits.

Conclusion

When comparing installment loans vs. payday loans, installment loans are almost always the safer, more affordable, and more manageable path for consumer borrowing. They offer lower relative APRs, longer repayment windows, and a structured system that actively reduces your debt with every payment. Avoid the lump-sum pressure of payday lending whenever possible to protect your financial stability.